Inner

City Press Community Reinvestment Report- December 19, 2005

Military personnel on active duty

are being overcharged on high interest loans by some of the largest banks in the

United States, a new

investigation of compliance with the Servicemembers’ Civil Relief Act (SCRA)

by Inner City Press has uncovered. Through documents

obtained under the Freedom of Information Act, Inner City Press has documented widespread

violations of the SCRA, defrauding and overcharging of those in active military

service, and regulatory inertia in dealing with the abuses. See also,

US soldiers’

families allege loan discrimination by HSBC," by Karl West, The Herald

(Glasgow, Scotland), December 5, 2005.

The nation’s largest bank,

Citigroup, is described in

consumers’ complaints as demanding original copies of initial deployment orders,

of refusing to deal by telephone with servicemembers’ immediate relatives, and

of reporting adversely to credit agencies.

HSBC / Household is

described as seeking to narrow SCRA’s interest rate reductions to only those “in

a hostile zone,” leaving that term undefined. Other banks most complained-of

include

JP Morgan Chase,

Wells Fargo, MBNA and

Bank of America.

The Servicemembers’ Civil Relief Act, at

50 USCS Appendix Section 527(1)(a) provides that

“An obligation or liability bearing interest at a rate in excess of 6 percent

per year that is incurred by a servicemember, or the servicemember and the

servicemember's spouse jointly, before the servicemember enters military service

shall not bear interest at a rate in excess of 6 percent per year during the

period of military service.”

The

purpose of the SCRA, formerly known as the Soldiers’ and Sailors’ Civil Relief

Act, is to provide interest rate relief and other protections “to

servicemembers of the United States to enable

such persons to devote their entire energy to the defense needs of the Nation.”

Section 502.

The above-named banks, however,

routinely seek to deny the SCRA protections to servicemembers. Citigroup, for

example, beyond deployment orders has demanded original enlistment papers, as

reflected in this complaint to

Citigroup’s AT&T Universal credit card unit in Jacksonville, Florida, now

placed online at

www.innercitypress.org/citiscra4.jpg

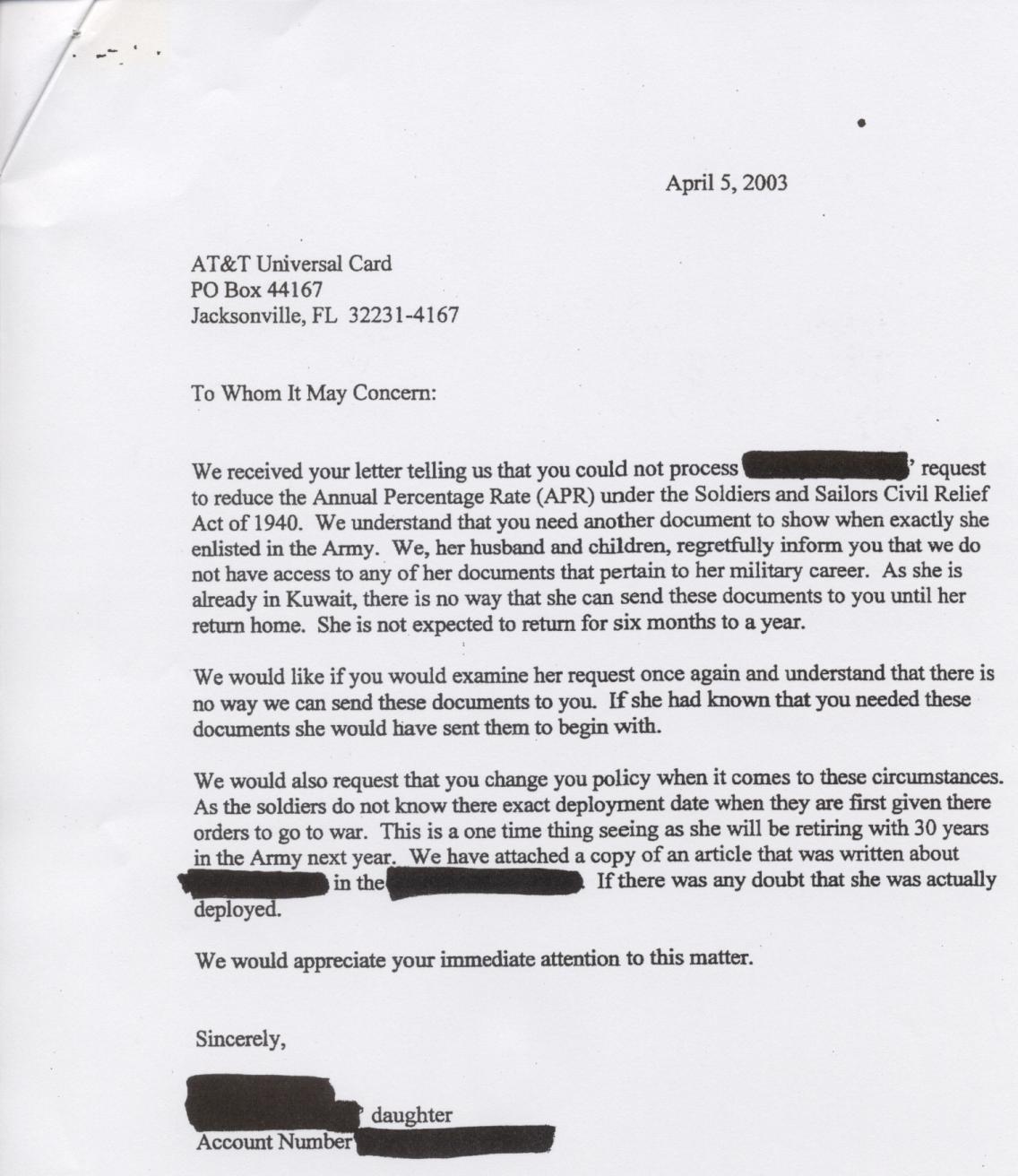

“We received your letter telling

us that you could not process [REDACTED]’s request to reduce the Annual

Percentage Rate (APR) under the Soldiers and Sailors Civil Relief Act of 1940.

We understand that you need another document to show when exactly she enlisted

in the Army. We, her husband and children, regretfully inform you that we do not

have access to any of her documents that pertain to her military career. As she

is already in Kuwait, there is no way that she can send these documents to you

until her return home. She is not expected to return for six months to a year.”

Using prior military service as an excuse to

maintain high interest rates despite the SCRA appears to the strategy as other

Citibank units as well, as reflected by the complaint to Citibank’s regulator,

the Office of the Comptroller of the Currency (OCC), now online at

www.innercitypress.org/citiscra4.jpg

“I am writing in regards to a

dispute with The Associates credit card company of Citicorp Credit Services,

Inc. (USA). The dispute pertains to my eligibility to receive the interest

credit from the Sailors’ and Soldiers’ Relief Act (SSCRA) (50 U.S. App. Sec.

526).

“I first contacted The

Associates in May of 2002. At that time I was denied enrollment. I was told that

because I originally entered the military in 1989, I was ineligible. However, my

tour of duty was over in 1993. I opened my account with The Associates in 2000.

At that time, I was a civilian and had no intentions of signing back up with the

military. Yet, in March of 2002, I entered into the US Army on full-time, active

military duty. As the law states, the SSCRA regulates the amount of interest I

am to be charged for any credit accounts I opened before entry into military

service.

"I have disputed this matter

with The Associates to no avail. I have sent them copies of my original orders

showing my current enlistment date, as well as a copy of the law. Still I was

denied. I was then forced to go to my JAG office on base to seek legal counsel.

From there I was directed to the Attorney General’s office in Irving, TX, the

headquarters for the aforementioned party. The Attorney General’s office then

put me in touch with the legal representatives of the [REDACTED] County, where I

received contact information for the OCC Customer Assistance Group.

"The Associates have repeatedly

denied my claims based on prior service. Yet, I have found nowhere in the law

where it states this as a deciding factor. So I write to you now, to examine the

law and enforce the necessary actions. I have enclosed all pertinent documents

in regard to this matter. I have been enrolled in a debt consolidation company,

and have made payments to The Associates monthly for the last year.”

The attachment, on Department of

the Army stationary, reflects Citigroup’s Associates charging 12.99% interest.

In April 2005, a mother wrote to the OCC, in a letter now online now online at

www.innercitypress.org/citiscra12.jpg

“Enclosed is a copy of my son’s military orders calling him

to active duty, a copy of the affidavit designating me as his authorized

representative, and a copy of my letter to Citibank, Sioux Falls, SD, dated 8

December, 2004. Citibank has given me all kinds of excuses for not acting on

this matter. First they wanted an affidavit specifically addressed to them. They

desisted on their request once I explained to them that the military do not have

the time and manpower to prepare affidavits in the manner Citibank wanted. Then

they told me that my son’s active duty orders were not with the correspondence I

had mailed them. Then they said I needed to prepare a document which they were

going to mail to me; I have never received such document. Last time I called I

was told that they were still investigating!”

Another mother complained:

…”His unit was deployed to the

Middle East. In February 2003 his fiancé and I applied to Citibank to have his

finance charges reduced under the Soldier’s and Sailor’s Relief Act of 1940.

(Account # [REDACTED]). We have supplied Citibank with several letters of proof

of my son’s service (copy of one enclosed) with no satisfaction. We recently

received a letter requesting a “Proof of Service Letter” from Citibank. While

the people at Citibank that I have spoken with are polite and helpful, nothing

has been accomplished. Telephone calls to the customer service number are no

help as the group that handles Soldier’s and Sailor’s Act requests are in

Jacksonville, FL and can’t be reached by telephone, only by mail. I think the

enclosed letter (which Citibank already has) from the Headquarters of II MEF

should be sufficient proof of my son’s service and that Citibank’s foot dragging

is nothing more than an attempt on their part to make the process so long and

drawn out so that we will give up as they do not want to lose the 24.24%

interest that is being paid on the account.”

Even when compliance is belatedly obtained from

Citigroup, accounts are

still turned over to collection agencies, and credit ratings impacted, as

reflected in this complaint to the FDIC, placed online at

www.innercitypress.org/citiscra5.jpg

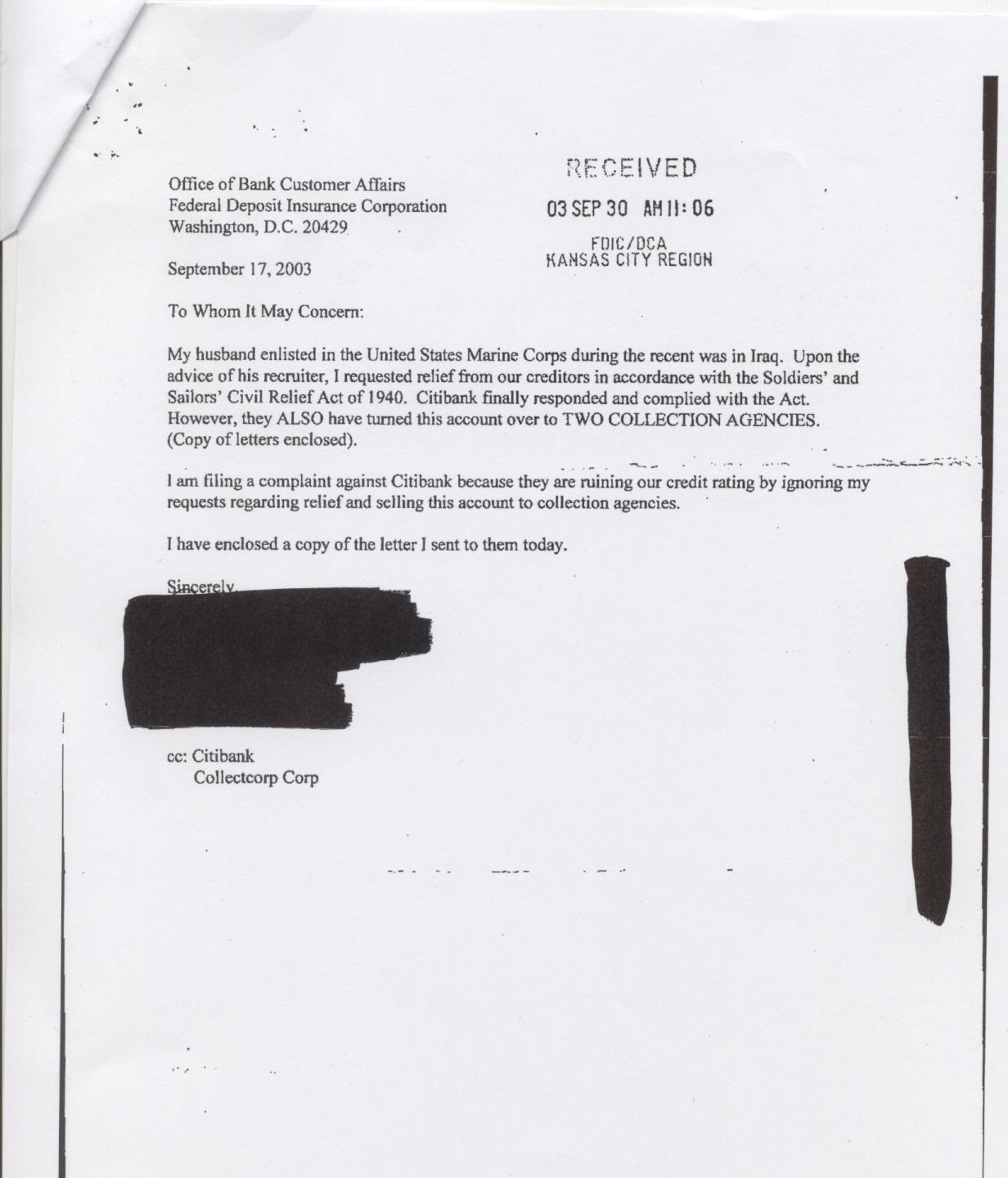

“My husband enlisted in the

United States Marine Corps during the recent war in Iraq. Upon the advice of his

recruiter, I requested relief from our creditors in accordance with the

Soldiers’ and Sailors’ Civil Relief Act of 1940. Citibank finally responded and

complied with the Act. However, they ALSO have turned this account over to TWO

COLLECTION AGENCIES (copy of letter enclosed).

“I am filing a complaint against

Citibank because they are ruining our credit rating by ignoring my requests

regarding relief and selling this account to collection agencies.”

The attached notice – even the name of the collection

agency has been redacted by the Office of the Comptroller of the Currency –

reflects a balance of $1,937.13. It begins: “This is to advise you that Citibank

(South Dakota) Na (P) has transferred your delinquent account to our office for

pre-legal collection.”

HSBC’s subprime consumer

finance units, operating under names including Household, HFC, Beneficial and

Orchard Bank, also stretch to find excuses to maintain high interest rates

contrary to the SCRA, as reflected by this sample complaint now online at

www.innercitypress.org/hsbcscra15a.jpg

and

www.innercitypress.org/hsbcscra15b.jpg

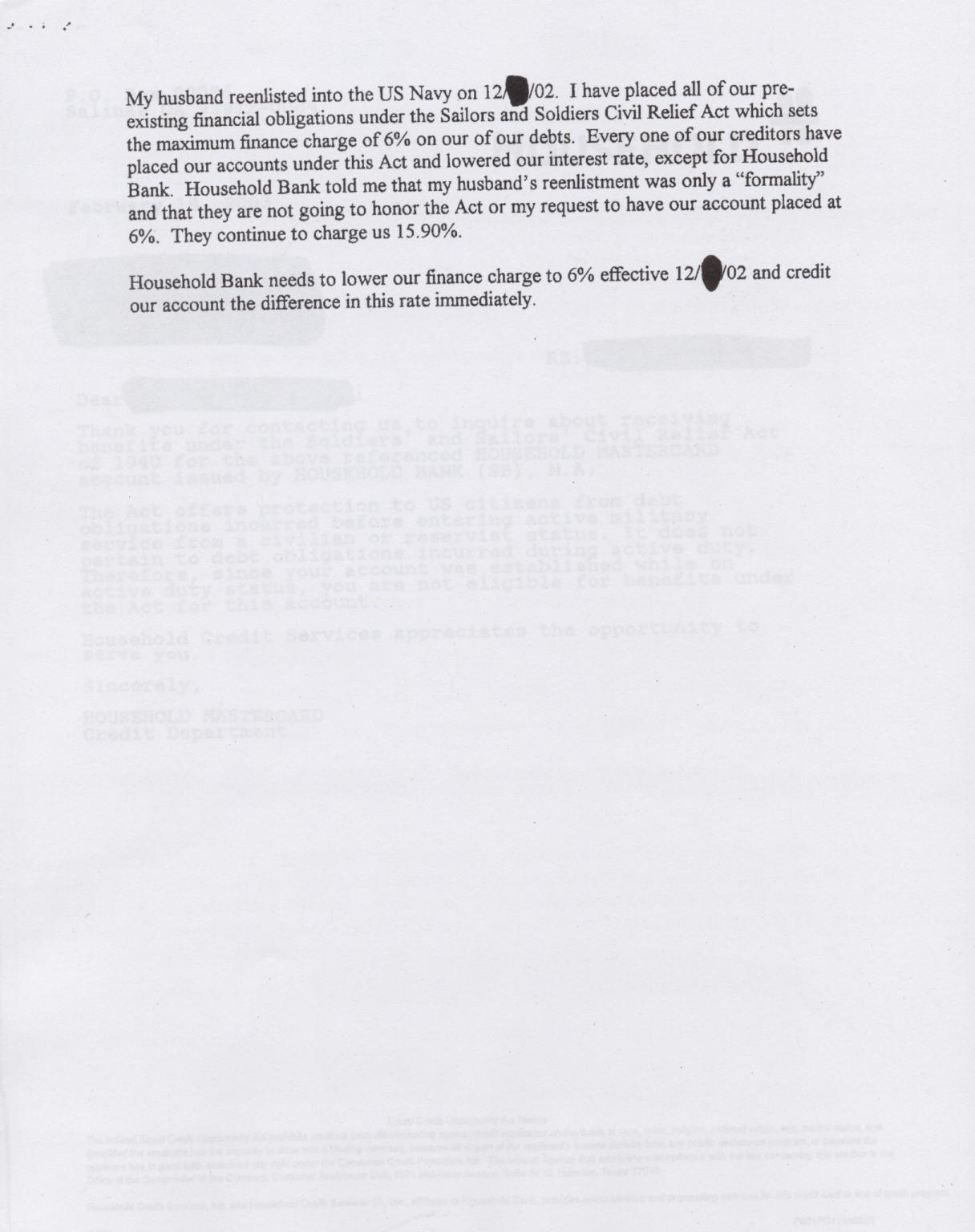

“My husband reenlisted into the

US Navy on 12/[ ]/02. I have placed all of our pre-existing financial

obligations under the Sailors and Soldiers Civil Relief Act which sets the

maximum finance charge of 6% on all of our debts. Every one of our creditors

have placed our accounts under this Act and lowered our interest rate, except

for Household Bank. Household Bank told me that my husband’s reenlistment was

only a ‘formality’ and that they are not going to honor the Act or my request to

have our account placed at 6%. They continue to charge us 15.90%.”

Contrary to the above-quoted language of the SCRA

(applying to “the period of military service”),

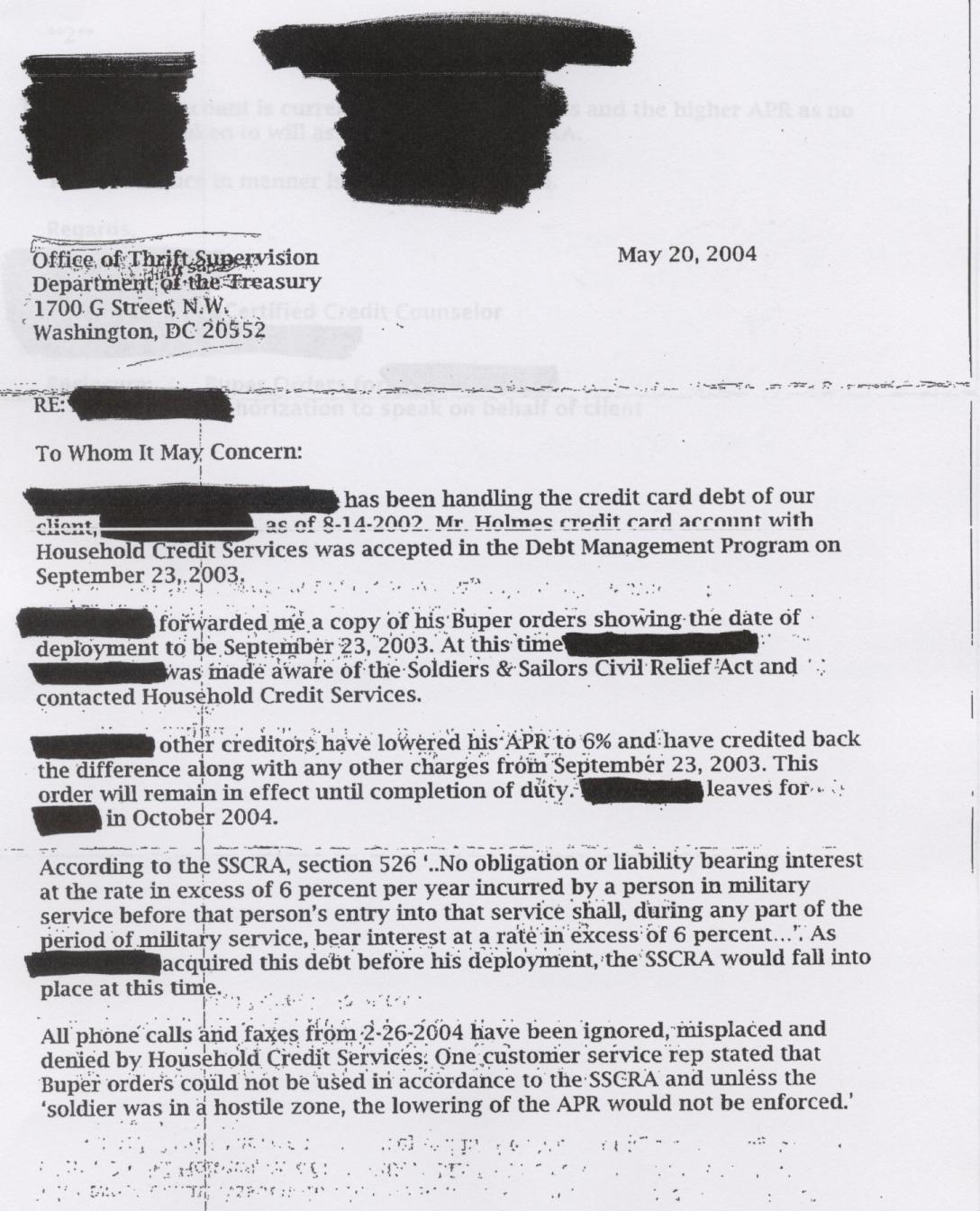

HSBC’s Household

came up with the novel argument, reflected in the complaint now online at

www.innercitypress.org/hsbcscra18.jpg

that the interest rate

must only be reduced if the soldier is in a “hostile zone” –

“All phone calls and faxes from

2-26-2004 have been ignored, misplaced and denied by Household Credit Services.

One customer service rep stated that Buper orders could not be used in

accordance to the SSCRA and unless the ‘soldier was in a hostile zone, the

lowering of the APR would not be enforced.’”

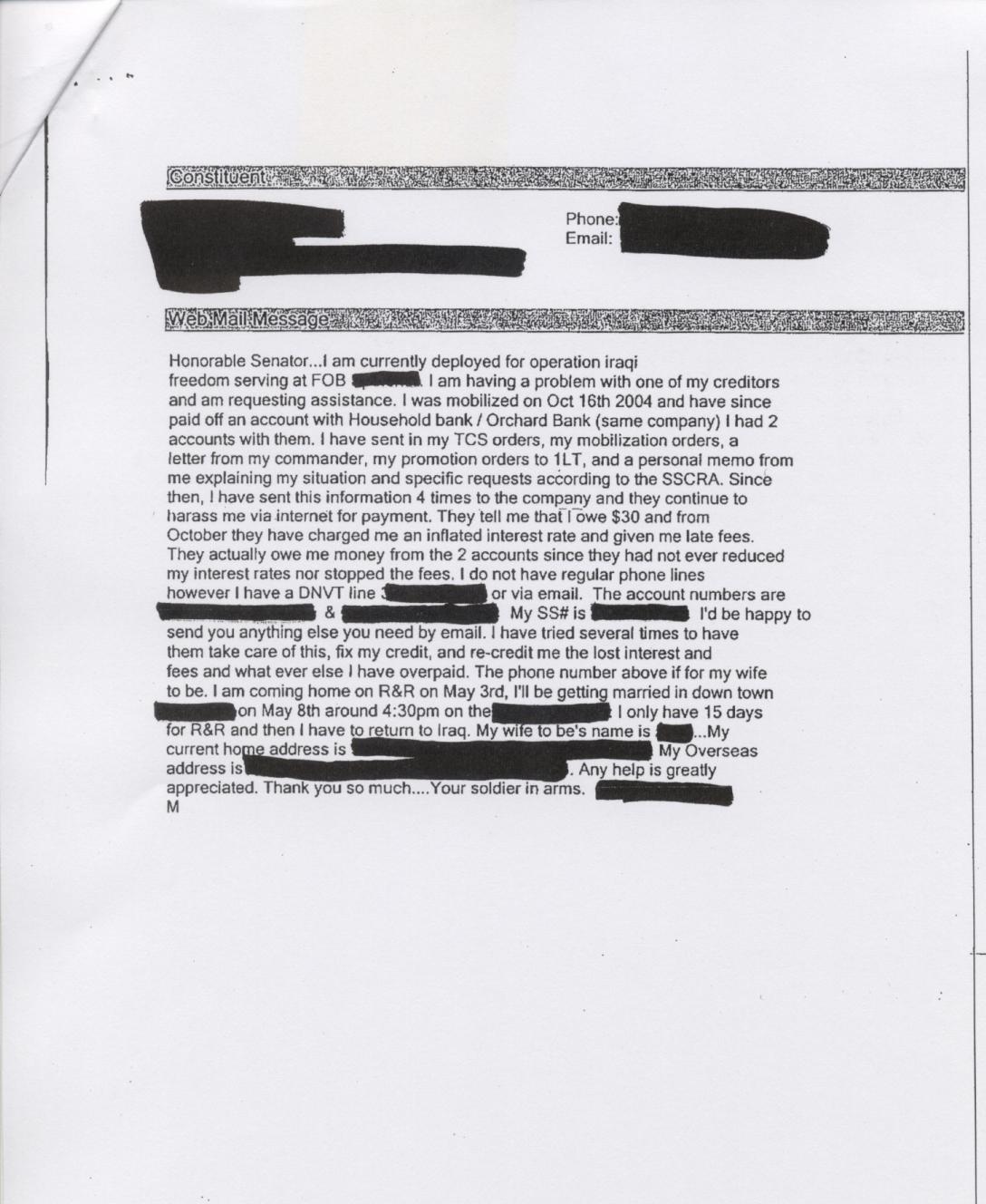

Even to those in “hostile zones,” HSBC sends bill

collection notices over the Internet, as reflected in the May 2005 complaint now

online at

www.innercitypress.org/hsbcscra22.jpg

“I am currently deployed for

operation Iraqi freedom serving FOB [REDACTED]. I am having a problem with one

of my creditors and am requesting assistance. I was mobilized on October 16,

2004 and have since paid off an account with Household Bank / Orchard Bank (same

company) I had 2 accounts with them. I have sent in my TCS orders, my

mobilization orders, a letter from my commander, my promotion orders to 1LT, and

a personal memo from my explaining my situation and specific requests according

to the SSCRA. Since then, I have sent this information 4 times to the company

and they continue to harass me via internet for payment. They tell me that I owe

$30 and form October they have charged me an inflated interest rate and given me

late fees. They actually owe me money from the 2 accounts since they had not

ever reduced my interest rates nor stopped the fees. I do not have regular phone

lines however I have a DNVT line [REDACTED] or via email…. Your soldier in

arms.”

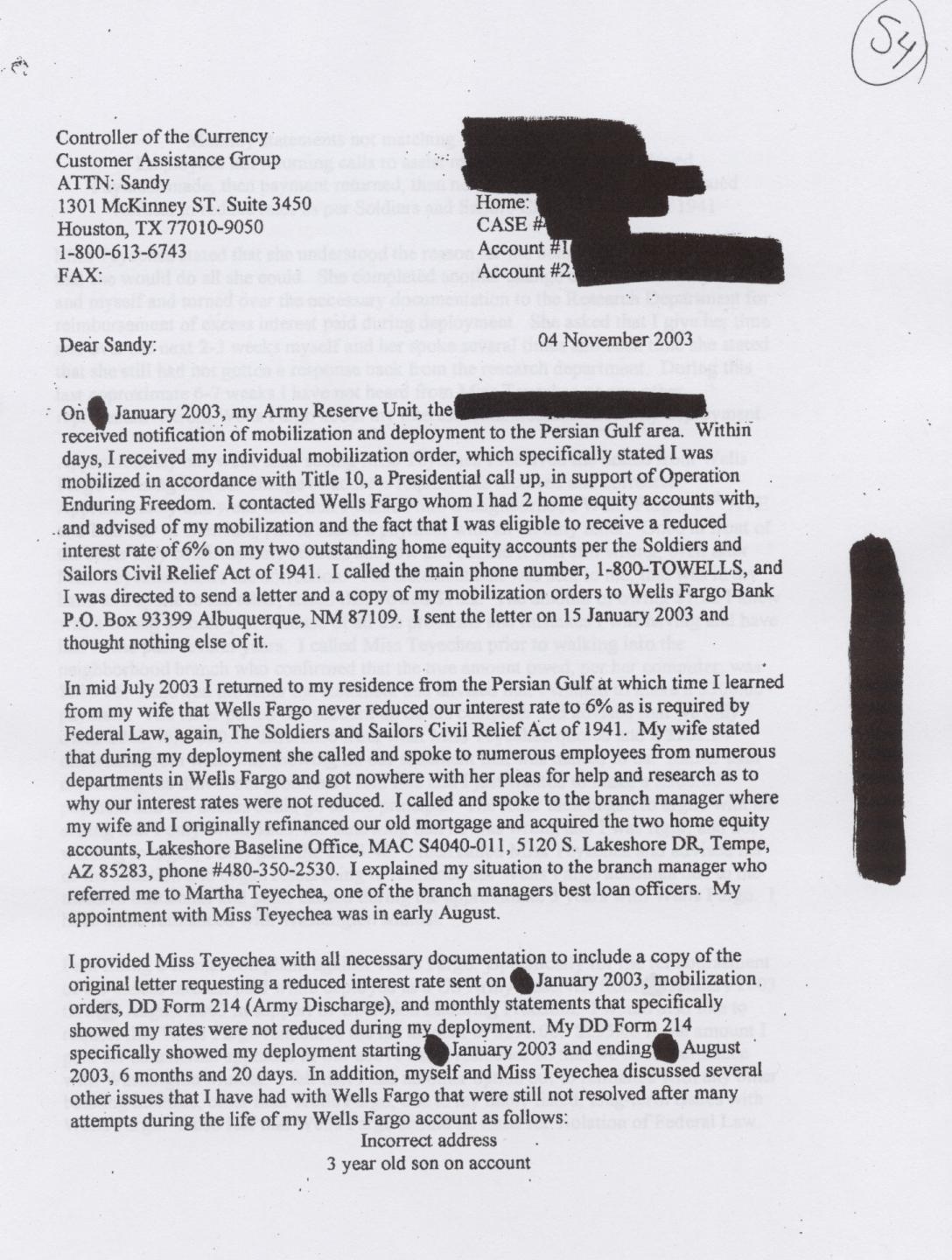

Wells

Fargo’s practices are reflected in the complaint to the OCC now online at

www.innercitypress.org/wellsscra54.jpg

“On [ ] January 2003, my Army

Reserve Unit, the [REDACTED] received notification of mobilization and

deployment to the Persian Gulf area. Within days I received my individual

mobilization order, which specifically stated I was mobilized in accordance with

Title 10, a Presidential call up, in support of Operation Enduring Freedom. I

contacted Wells Fargo whom I had 2 home equity accounts with, and advised of my

mobilization and the fact that I was eligible to receive a reduced interest rate

of 6% on my two outstanding home equity accounts per the Soldiers and Sailors

Civil Relief Act of 194[0]… In mid July 2003 I returned to my residence from the

Persian Gulf at which time I learned from my wife that Wells Fargo never reduced

our interest rate to 6% as is required by Federal law…”

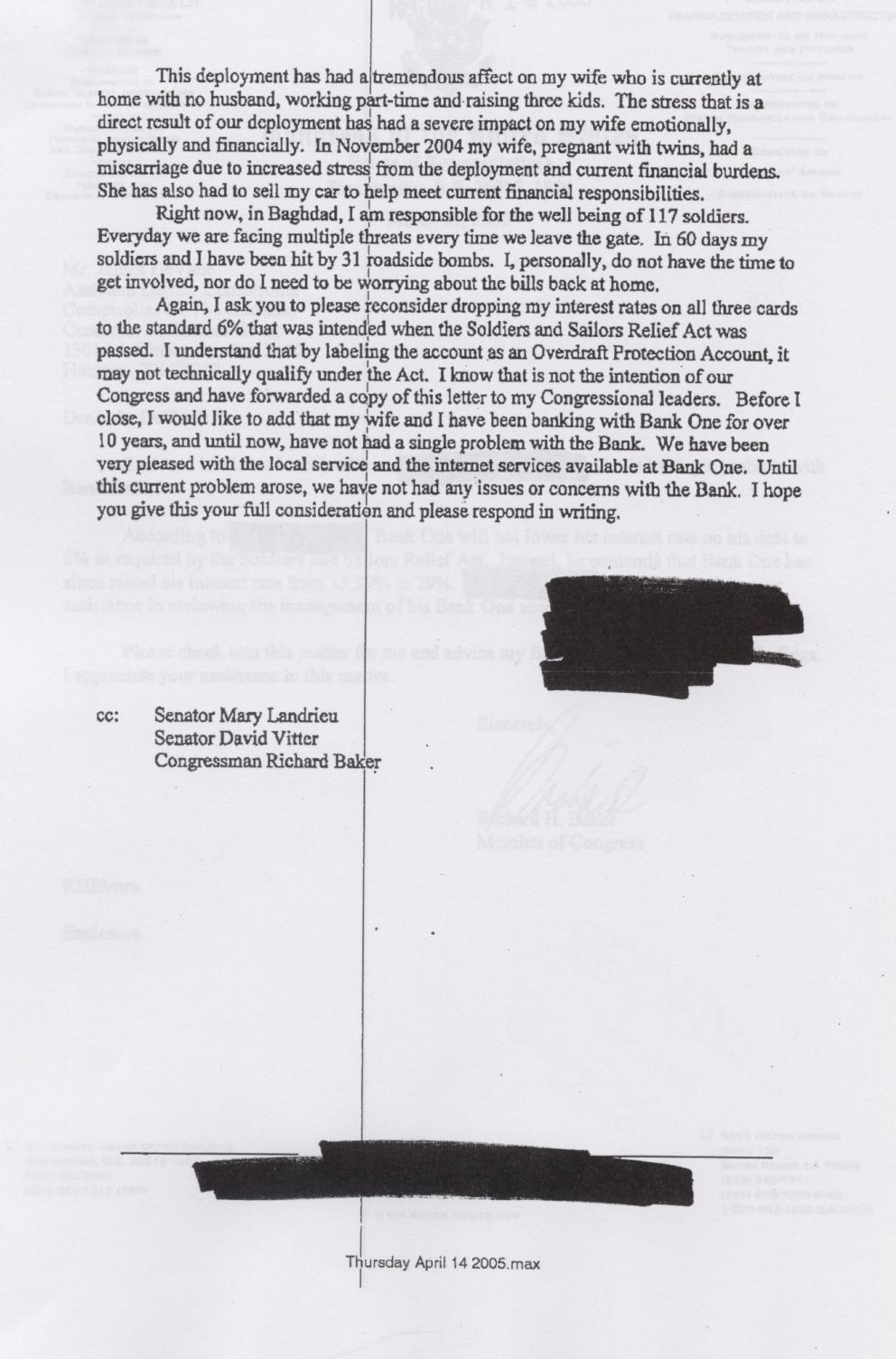

JP

Morgan Chase’s practices, and their impact on front-line military personnel,

are reflected in the complaint now online at

www.innercitypress.org/jpmcscra47a.jpg and

www.innercitypress.org/jpmcscra47b.jpg

“I am writing you from Baghdad,

Iraq asking, once again, for Bank One to drop my interest rate on these three

cards to 6%. I have phoned in and spoken with your customer service on two

previous occasions, once in May 2004 when my deployment began, and again in

September 2004, before I actually deployed to Iraq. Both times I was instructed

by the customer service that because the three accounts in question were for

Overdraft Protection, they did not qualify under the Soldiers and Sailors Relief

Act. This makes no sense to me, considering the accounts are clearly operated

like a credit card. I have used these accounts to complete balance transfers,

operate as a Visa credit card, and for overdraft protection. It is clear that

even though the account functions as a credit card, Bank One is using the

technicality of it being classified as an Overdraft Protection to ensure that

soldiers like me cannot benefit from the Soldiers and Sailors Relief Act on

these type of accounts. I am asking you to please reconsider. The following

three accounts in question are as follows:

Account 1 [REDACTED] 13.99%

interest

Account 2 [REDACTED] 28.99%

interest

Account 3 [REDACTED] 13.99%

interest

…In November 2004 my wife,

pregnant with twins, had a miscarriage due to increased stress from the

deployment and current financial burdens. She has also had to sell my car to

help meet current financial responsibilities. Right now, in Baghdad, I am

responsible for the well being of 117 soldiers. Everyday we are facing multiple

threats every time we leave the gate. In 60 days my soldiers and I have been hit

by 31 roadside bombs. I, personally, do not have the time to get involved, nor

do I need to be worrying about the bills back home.”

The purpose of the Servicemembers’ Civil Relief

Act is to provide interest rate relief and other protections “to

servicemembers of the United States to enable

such persons to devote their entire energy to the defense needs of the Nation.”

50 USCS Appendix Section 502. Given the

lack of compliance with the SCRA by the above-named largest banks and bank

holding companies, Inner City Press will be redoubling its reporting on this

issue.

©opyright 2006 Inner City Press, Inc. To request

reprint or other permission, e-contact Editors [at] innercitypress.com - phone: (718) 716-3540

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}